We'll also set a temporary cookie to hide this notice.

21

Mar

2024

Lee Cooper | Industry and Strategy Lead

In this series of articles, Lee Cooper, Industry and Strategy Lead at Link Group, looks at the forthcoming digitisation of the UK shareholding framework, and sets out his considerations around the implications of proposed digitisation models, and which will be most suitable for companies, practitioners, and shareholders.

As part of their remit to modernise the UK’s shareholding framework, the Digitisation Taskforce is looking at solutions to removing paper, including certificates, from share ownership or the transfer process, digitising communications as well as other processes. The Taskforce issued an Interim Report in 2023 and invited comments from stakeholders across the financial services sector on the proposals they made to dematerialise the market.

The main proposal from the Taskforce was that current certificated shareholders (circa. 10 million individuals) would need to transfer their holdings into an intermediated model administered by a nominee. The details of shareholders would no longer be held by the issuer companies but by external nominees such as those administered by stockbrokers. This potential future model has been called the intermediated model or model 3.

The other main model for future dematerialisation of shares that was considered, but rejected, by the Taskforce, was based on removing paper share certificates but leaving the shareholder records on the existing share registers of the issuer companies and removing other barriers to digitisation. This has been called the digital register or model 1.

The proposals are not detailed yet, but we thought it would be helpful to try and appreciate the implications of the changes and how the changes might impact shareholders, issuer companies and the securities market as a whole.

Initially we looked at the implications for shareholders and issuer companies of moving to the intermediated model compared to the digital register model, here we look at the possible costs associated with both dematerialisation models.

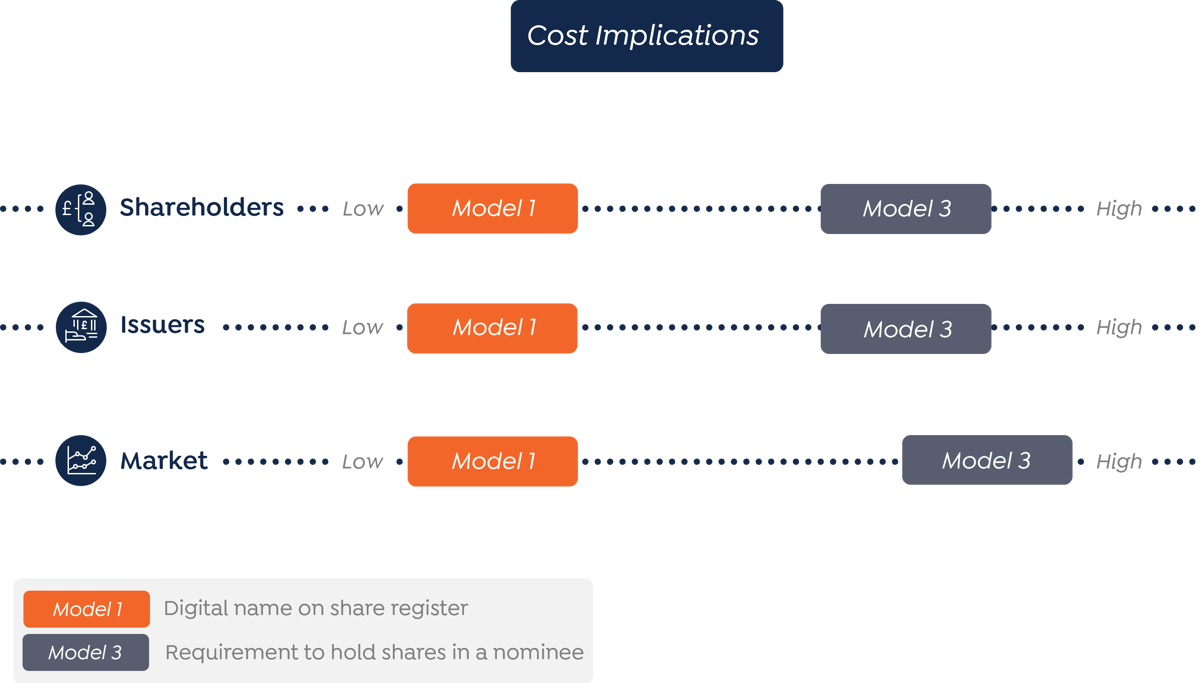

Shareholder cost impacts

There is currently no cost for shareholders to hold their shares in certificated form, which would continue under the digital register model. However, this would be replaced by optional contractual services at cost to the shareholder under the intermediated model. Where shareholders are unable to produce share certificates to transfer holdings into an intermediated nominee, there are currently costs to provide certificate indemnities.

Unless law or regulation provides new protections, shareholdings in the intermediated model may be at risk if a nominee administrator/broker goes into default. Under the intermediated model, shareholders who do not respond to the change and fail move to a nominee arrangement risk losing the shares they own as the current proposals suggest that such shares are forfeit after an agreed period.

Issuer company costs

A significant percentage of issuer costs relate to corporate communication obligations - quicker and more substantive issuer savings can be made by simply changing the communications default under the digital register model to electronic communications.

Nominee arrangements come with more extensive obligations and oversight – consequently this arrangement is more expensive to administer than the digital register option.

Also, arrangements for residual shareholders who do not/cannot appoint a nominee will probably need to be met by the issuer company.

The intermediated model is expected to require substantial legal and regulatory changes to enable its delivery which is likely to be more extensive and costly than those required for the digital register model. New technology systems required will also add to the cost of change. Below we have tried to represent the different cost challenges of the dematerialisation proposals.

In our next and final article we will look at the likely transition and delivery timetable to implement the models for dematerialisation. You can also read part 1 of this series by clicking here.

If you’ve found this article useful, and want to share your thoughts with our experts – please get in touch.

© 2024 Link Market Services. All rights reserved.

Legal and Policies

Quick links

Please read our cookie notice for full details of the types and details of cookies used on this website or to change your cookie settings.

Link Group is a trading name of Link Market Services Trustees Limited which is authorised and regulated by the Financial Conduct Authority and which is also authorised to conduct cross-border business within the EEA under the provisions of the EU Markets in Financial Instruments Directive.

A division of MUFG Pension & Market Services